How It Works

Understanding Namibia's Instant Payment Solution

Overview

A National Digital Payments Platform

Instant Payments Namibia operates Namibia's Instant Payment Solution, a shared national platform that allows money to move instantly between participating banks, mobile money providers, and other licensed payment service providers.

Rather than replacing existing banking or mobile payment apps, the system connects them. It acts as a common backbone that enables different providers to speak to one another in real-time, safely and at low cost.

The Process

The Basic Idea

At its core, the system works as follows:

- Payment initiated via bank app, mobile wallet, or USSD

- Payment routed through IPN's national platform

- Money received instantly, regardless of bank or wallet

- Both parties receive instant confirmation

This happens within seconds, at any time of day, including weekends and public holidays.

Accessibility

Designed for Inclusivity

Digital payments are now accessible to all Namibians, including those who:

- Do not own smartphones

- Live far from bank branches or ATMs

- Rely on mobile wallets rather than traditional bank accounts

- Operate in the informal or small business sector

- Access payments via mobile, USSD, and banks, with cash-in/out support that lowers barriers to the digital economy

Inclusivity is a central objective of the Instant Payment Solution.

Connectivity

Interoperability at the Core

The system makes it possible for:

- A bank customer to send money to a mobile wallet user

- A mobile money user to pay a merchant who banks elsewhere

- Government payments to be received into different types of accounts

- Businesses to pay individuals without worrying about which provider they use

- Common rules, standards, and a central switching infrastructure ensure seamless, fair, and reliable payments across all providers

This removes the need for multiple closed systems and reduces friction for users.

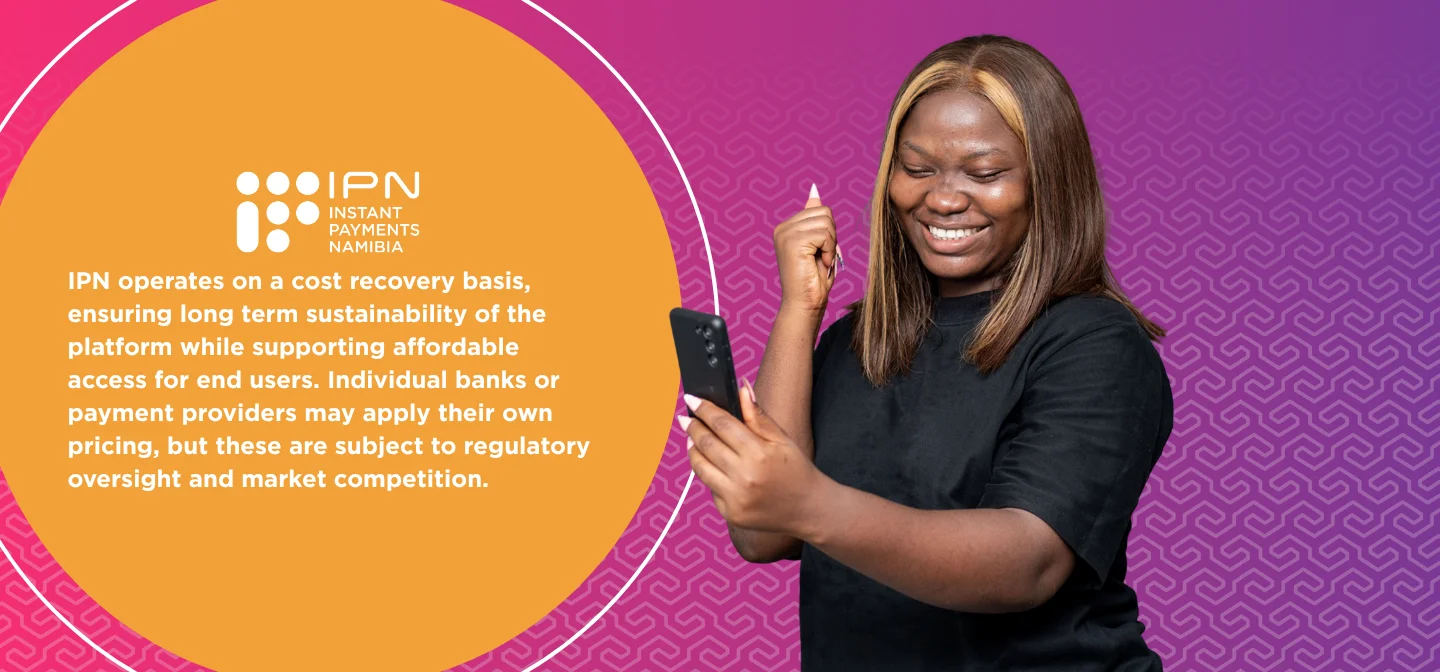

Affordability

Simple and Transparent Fee Structures

Key principles guiding the fee structure include:

- Affordable payments designed for everyday transfers and small transactions

- Fees are charged at the infrastructure level, not by IPN directly to the public

- Costs are transparent and known in advance

- Fees are aligned with the actual cost of operating the system

- Lower value, high frequency transactions are prioritised for affordability

Cost-recovery ensures sustainability while regulation and competition keep pricing fair and accessible.

Protection

Safety, Security, and Trust

- Every transaction is protected by multi-layered security and risk controls

- Strong authentication of users by their payment provider

- Real-time monitoring for fraud and unusual activity

- Clear rules for dispute handling and transaction reversals where applicable

- High system availability and resilience standards

- Built in close collaboration with regulators and industry to ensure a secure, reliable, and trusted national payment infrastructure

Public Infrastructure

A Shared National Asset

IPN's role is to ensure that the platform remains:

- Neutral and fair to all participants

- Open to innovation and future use cases

- Scalable as volumes and usage grow

- Aligned with Namibia's broader digital and financial inclusion goals

- A shared national payment infrastructure, not owned or controlled by any single institution

National Impact

What This Means for Namibia

By enabling instant, affordable, and interoperable payments, the system supports:

- Greater financial inclusion

- Reduced reliance on cash

- Improved efficiency for businesses and government

- Increased trust in digital financial services

Ultimately, the Instant Payment Solution is about making everyday payments simpler, faster, and more accessible for everyone in Namibia.

Getting Involved

Participation in the Instant Payment Solution

Who Can Join

The Instant Payment Solution is open to licensed banks and payment service providers operating in Namibia that meet regulatory, technical, and risk requirements.

Participation is governed by national payment regulations and overseen by the Bank of Namibia, with onboarding and system access managed by Instant Payments Namibia (IPN). The platform follows a multi-tier participation model, allowing different types of institutions to take part based on their role and capability.

Store of Value (SoV) Providers

These are institutions that hold customer funds and provide the accounts or wallets used to send and receive money.

SoV Providers:

- Open and manage customer accounts or e-wallets

- Hold funds on behalf of users

- Receive and process real-time debit and credit instructions

- Confirm transactions instantly

Only licensed banks and licensed non-bank Payment Instrument Issuers may act as Store of Value Providers.

Instant Payment Service Providers (IPSPs)

These are entities that connect directly to the national IPS platform and send or receive payment instructions.

IPSPs:

- Integrate with the IPS switch

- Initiate or receive instant payments for customers

- Follow common technical standards, messaging rules, and service levels

- Maintain high availability and security

An organisation may act as both an SoV Provider and an IPSP, provided it meets the requirements for each role.

Regulatory Eligibility

Only entities that are:

- Licensed under Namibia's payment system regulations, and

- Authorised by the IPS Operator,

may participate in the Instant Payment Solution. Before engaging IPN, all applicants must first obtain regulatory clearance from the Bank of Namibia.

How the Application Process Works

Participation follows a clear, structured pathway through five key stages, from initial regulatory clearance to final approval and admission into the ecosystem.

Regulatory Clearance

The applicant submits a formal letter of intent to the Bank of Namibia. If approved, the Bank issues a letter of no objection.

Engagement with IPN

With this clearance, the applicant formally engages IPN and signs a confidentiality agreement. IPN then provides the technical and functional specifications needed for integration.

Formal Application

The applicant submits a membership application to IPN, including proof of licensing, intended role, governance and compliance information, and technical readiness.

Testing and Certification

Applicants must complete system integration testing, live transaction testing, settlement and messaging validation, and final certification.

Final Approval

IPN submits its recommendation to the Bank of Namibia for endorsement. Once endorsed, the applicant is formally admitted into the IPS ecosystem.

Transparency and Oversight

All participation decisions are:

- Subject to regulatory endorsement

- Based on technical capability, financial soundness, and risk readiness

- Communicated formally and transparently

Applicants whose submissions are not approved may appeal through the Bank of Namibia.

Why This Matters

A Fair and Trusted National Payments Ecosystem

This structured participation model ensures that the Instant Payment Solution delivers broad, long-term benefits for Namibia.

- All participants meet the same standards and obligations, regardless of size.

- Consumers are protected through clear rules, oversight, and strong risk management.

- The system remains safe, reliable, and trusted as usage and transaction volumes grow.

- Innovation is encouraged while maintaining overall stability and public confidence.

The result is a fair, open, and future-ready national payments ecosystem that works for everyone.

Become a Participant